1.3 Purpose of this User Manual

1.4 Who Should Use This Manual

1.4 Best Practices and System Limitations

1.4.1 Setting up the Master Files

4.1.1.1 How to Add an Item Manually

4.1.1.2 Add Item Via Import Function

4.1.2.2 Add Customer Via Import Function

4.1.3.2 Add Supplier Via Import Function

List of All Users that were added to the System

4.1.6.1 Chart of Accounts Lists

4.1.6.2 Manual Add Chart of Accounts

4.1.6.2 Add Chart of Accounts via Upload Account

4.1.8.2 Manual Add of Currency

4.2.1.1 Manual Update Item Detail

4.2.1.2 Update Item Detail in Bulk

4.2.2.1 Manual Update Supplier Detail

4.2.2.1 Update Supplier Detail in Bulk

4.2.3.1 Manual Update Customer Detail

4.2.3.1 Update Customer Detail in Bulk

5.2 Purchases Transaction Module

Cancel Purchase Request Transaction

Purchase Order Transaction via Upload Template

Cancel Purchase Order Transaction

Cancel Receiving Receipt Transaction

Cancel Disbursement Transaction

Debit Memo Transaction via Upload Template

Sales Order Transaction via Upload Template

Cancel Sales Order Transaction

Sales Invoice Transaction via Upload Template

Cancel Sales Invoice Transaction

Collection Transaction via Upload Template

Scenario 3: Extra-Ordinary Activities

Scenario 4: Multi-Branch with EasyPOS Integration

Accounts Payable Voucher Report

Accounts Payable By Currency Report

Purchase Request Summary Report

Purchase Request Detail Report

Purchase Order Detail With Balance Report

Receiving Receipt Summary Report

Receiving Receipt Detail Report

Print or Download the PDF Report

Available Item Per Batch Report

Cancelled Purchase Request Report

Cancelled Purchase Order Report

Cancelled Receiving Receipt Report

Accounts Receivable Summary Report

Accounts Receivable by Term Report

Accounts Receivable by Currency Report

Accounts Receivable Report (One Month)

Statement of Account (By Date Range)

Collection Summary by PayType Report

Cancelled Sales Invoice Report

Sales Invoice Detail Report with Cost

Stock Transfer Detailed Report

13.1.1 Benefits of Integration

13.2.1 EasyPOS Integration Overview

13.3 How to Set Up Integrations

.toc-wrapper .c27{margin-left: 6pt}.toc-wrapper .c46{margin-left:14pt}.toc-wrapper .c46 .c14 a,.toc-wrapper .c50 a{font-size:13px}.toc-wrapper .c50{margin-left:18pt;} .manual-content table td, .manual-content table th{padding:0;border: 1px #aaa solid;padding: 10px;} .manual-content table td span,.manual-content table td p,.manual-content table td li{font-size:11px!important;}Form 2306 is a tax document issued by the Bureau of Internal Revenue (BIR) in the Philippines, certifying the amount of final tax withheld on certain income payments. It applies to specific types of income subject to final withholding tax, such as dividends, royalties, and interest. The form contains details about the withholding agent and the income recipient, as well as information on the nature and amount of income paid, the tax rate applied, and the amount of tax withheld. It serves as proof of tax compliance for the income recipient, ensuring accurate tax reporting and aiding in personal or corporate tax filings.

To generate Form 2306, here are the steps to follow:

NOTE: Shall be issued to payee on or before January 31 of the year following the year in which income payment was made. However upon request of the payee the payor must furnish such statement to the payee simultaneously with the income payment.

Source: https://www.bir.gov.ph/index.php/bir-forms/certificates.html

Form 2307 is a tax document issued by the Bureau of Internal Revenue (BIR) in the Philippines, certifying the amount of creditable tax withheld at source on certain income payments. It applies to various types of income subject to withholding tax, such as professional fees, commissions, and rental payments. The form includes details about the withholding agent and the income recipient, along with information on the nature and amount of income paid, the tax rate applied, and the amount of tax withheld. This certificate is used by the income recipient to claim the withheld tax as a credit against their tax liability, ensuring accurate tax reporting and compliance during the filing of tax returns.

To generate Form 2307, here are the steps to follow:

Note: For EWT – Shall be issued to payee on or before the 20th day of the month following the close of the taxable quarter. Upon request of the payee, however, the payor must furnish such statement to the payee simultaneously with the income payment.

For Percentage Tax On Government Money Payments – Shall be issued to the payee on or before the 10th day of the month following the month in which withholding was made. Upon request of the payee, however, the payor must furnish such statement to the payee simultaneously with the income payment.

For VAT Withholding – Shall be issued to the payee on or before the 10th day of the month following the month in which withholding was made. Upon request of the payee, however, the payor must furnish such statement to the payee simultaneously with the income payment.

Source: https://www.bir.gov.ph/index.php/bir-forms/certificates.html

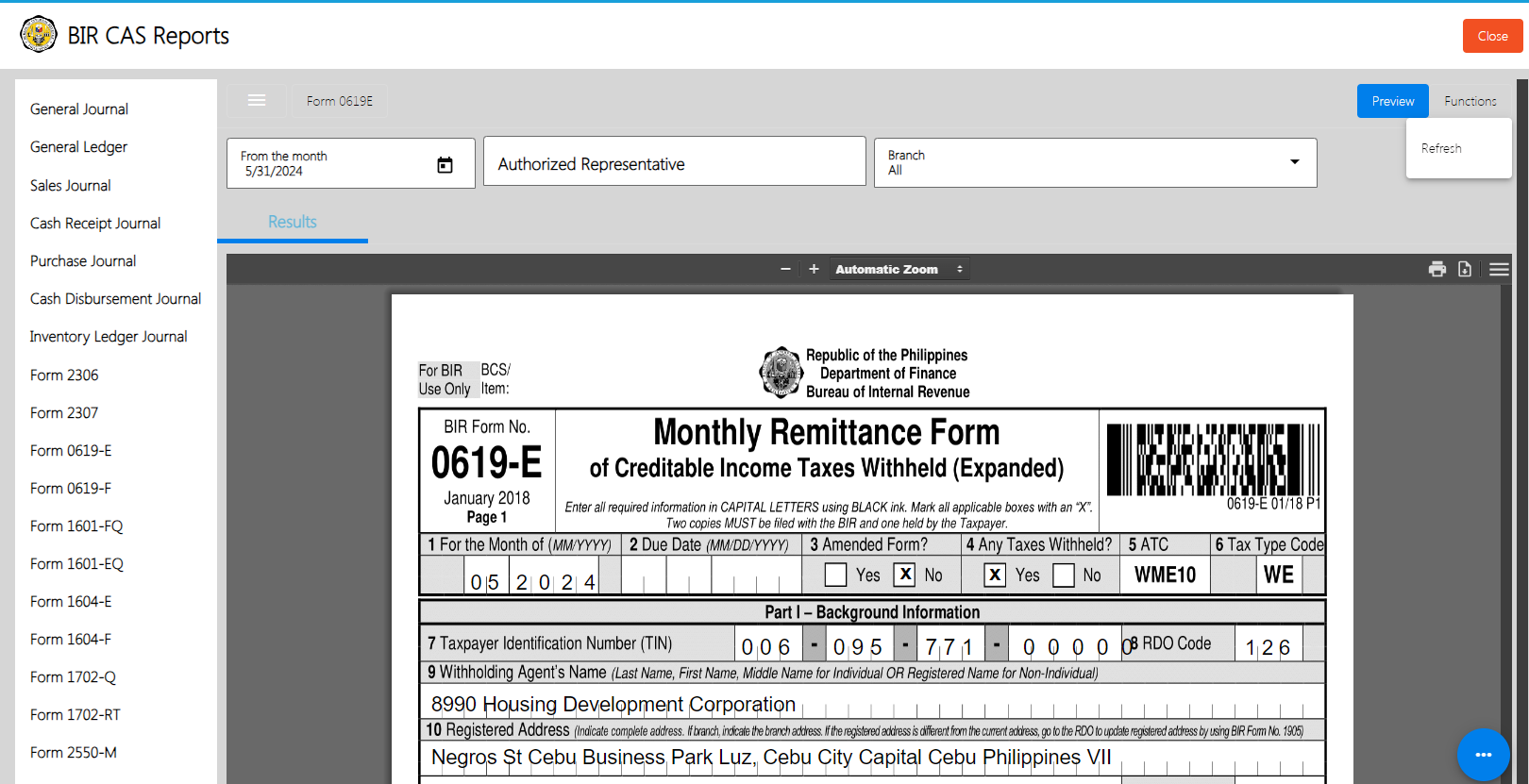

Form 0619-E is a tax document issued by the Bureau of Internal Revenue (BIR) in the Philippines, used for remitting creditable withholding taxes expanded (EWT) on specific income payments for a particular month. It applies to various payments such as professional fees, rentals, and commissions. The form includes details about the withholding agent, such as name, Taxpayer Identification Number (TIN), and address, and summarizes the income payments and taxes withheld. It ensures that withholding agents report and remit the correct amount of creditable withholding tax, aiding in accurate tax reporting and compliance for both the withholding agent and the income recipients.

To generate Form 0619 – E, here are the steps to follow:

Note: Deadline – Every 10th day of after the end of each month

Requirement – Monthly Remittance Form for Creditable Income Taxes WIthheld (Expanded)

Source: http://www.cleodu-cpas.com/index.php/bir-tax-deadlines

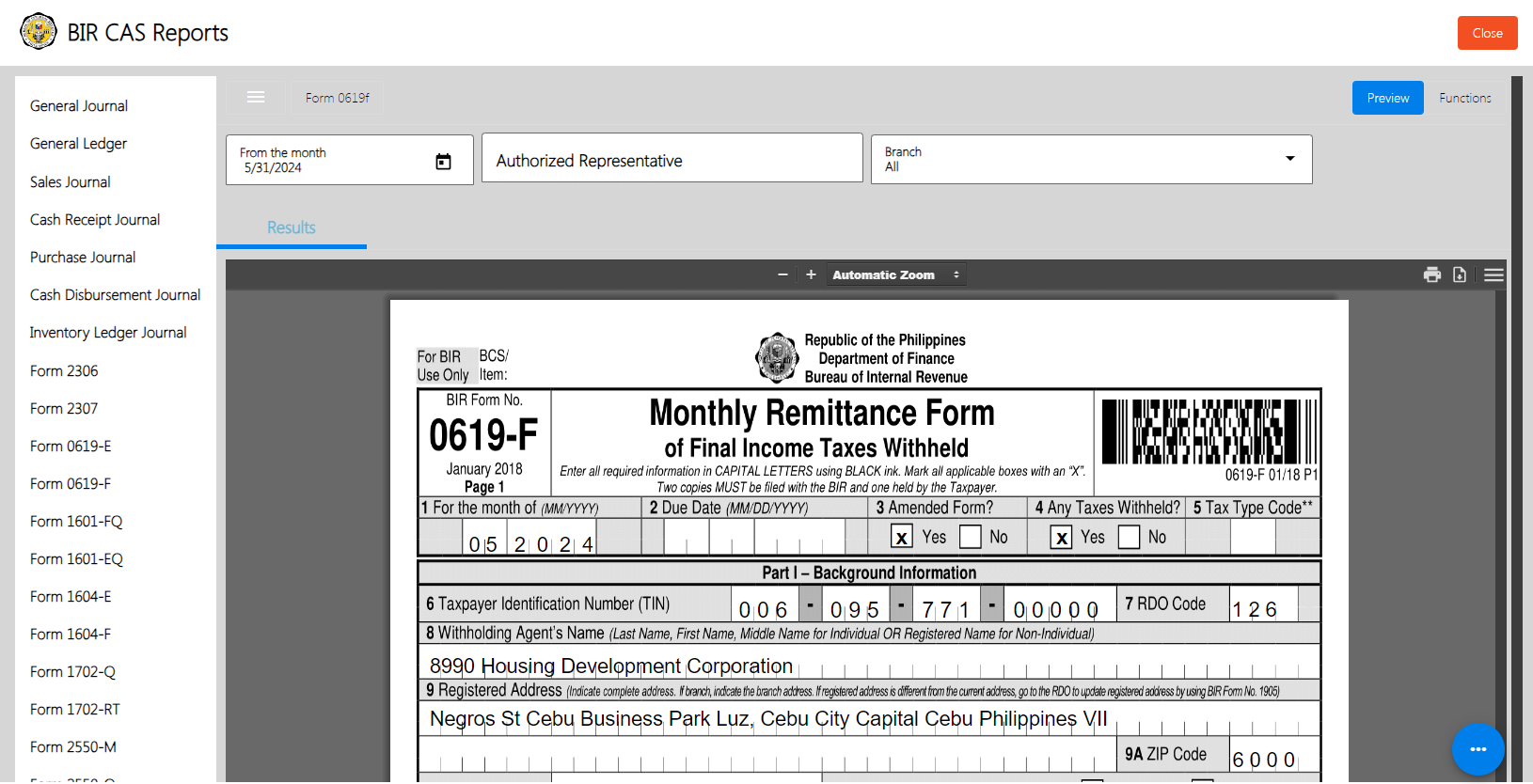

Form 0619-F is a tax document issued by the Bureau of Internal Revenue (BIR) in the Philippines, used for remitting final withholding taxes on certain income payments for a specific month. This form is utilized by withholding agents who deduct and remit taxes on income subject to final withholding tax, such as interest, dividends, and other specified payments. It includes details about the withholding agent, such as name, Taxpayer Identification Number (TIN), and address, and provides a summary of the income payments and the final taxes withheld. BIR Form 0619-F ensures that withholding agents correctly report and remit the final withholding taxes, facilitating accurate tax reporting and compliance for both the withholding agent and the income recipients.

To generate Form 0619 – F, here are the steps to follow:

Note: Deadline – Every 10th day of after the end of each month

Requirement – Monthly Remittance Form for Final Income Taxes Withheld

Source: http://www.cleodu-cpas.com/index.php/bir-tax-deadlines

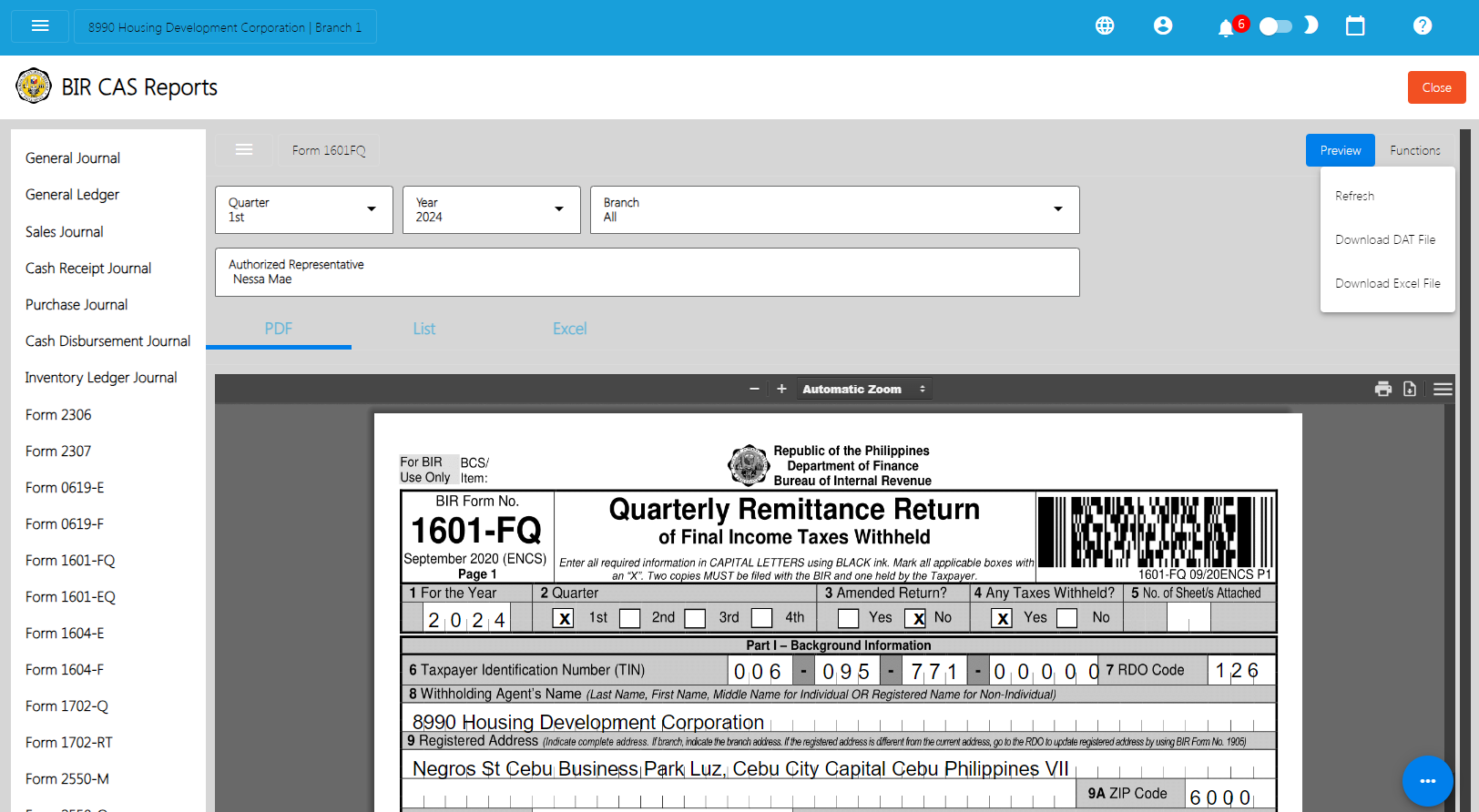

Form 1601-FQ is a tax document issued by the Bureau of Internal Revenue (BIR) in the Philippines, used for the quarterly remittance of final withholding taxes. This form is used by withholding agents to report and remit taxes withheld on income payments subject to final withholding tax, such as interest, royalties, dividends, and other specified payments, for each quarter. It includes details about the withholding agent, such as name, Taxpayer Identification Number (TIN), and address, and provides a summary of the income payments and final taxes withheld for the quarter. BIR Form 1601-FQ ensures that withholding agents accurately report and remit the final withholding taxes on a quarterly basis, aiding in tax compliance and accurate reporting for both the withholding agent and the income recipients.

To generate Form 1601 – FQ, here are the steps to follow:

Note: Deadline – Every Last Day of the month after the end of each quarter

Requirement – Quarterly Remittance Return of Final Income Taxes Withheld

Source: http://www.cleodu-cpas.com/index.php/bir-tax-deadlines

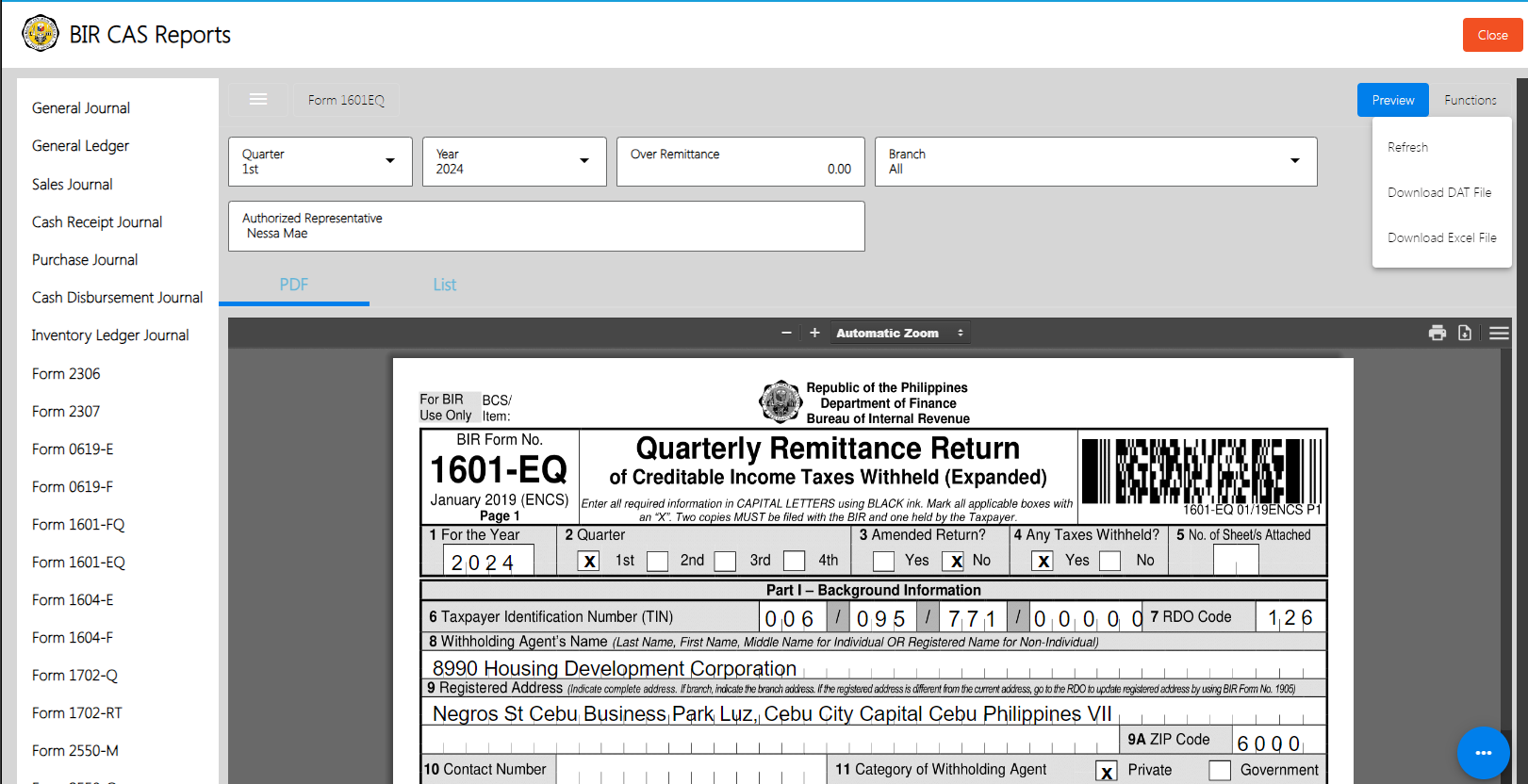

Form 1601-EQ is a tax form used in the Philippines for the quarterly filing of creditable withholding taxes. This form is designed to report and remit taxes withheld by a payor (withholding agent) from various income payments made to individuals and businesses. The EQ in the form’s name stands for “Expanded Quarterly,” indicating its use for expanded withholding tax purposes. The form ensures compliance with the Bureau of Internal Revenue (BIR) regulations, helping to accurately document and pay the taxes withheld on payments such as professional fees, commissions, and rental income, among others.

To generate Form 1601 – EQ, here are the steps to follow:

Note: Deadline – Every Last Day of the month after the end of each quarter

Requirement – Quarterly Remittance Return of Creditable Income Taxes Withheld (Expanded) (together with the Quarterly Alphabetical List of Payees)

Source: http://www.cleodu-cpas.com/index.php/bir-tax-deadlines

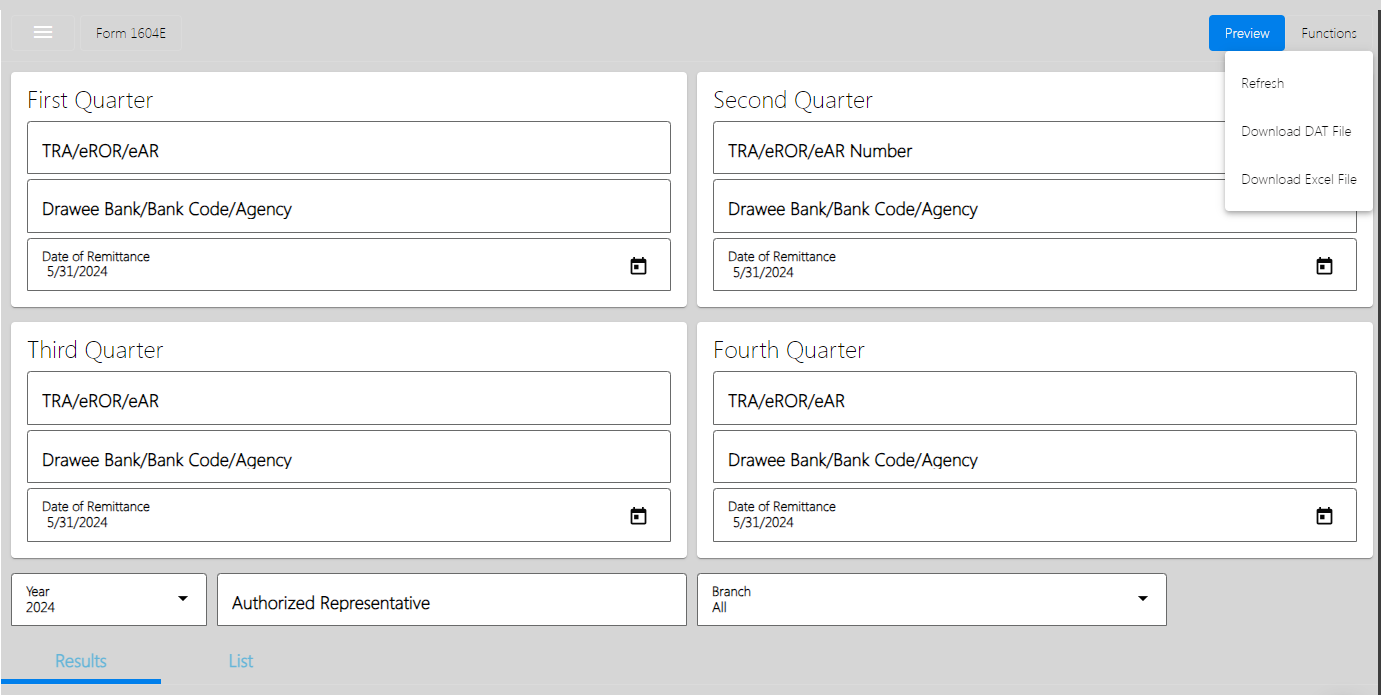

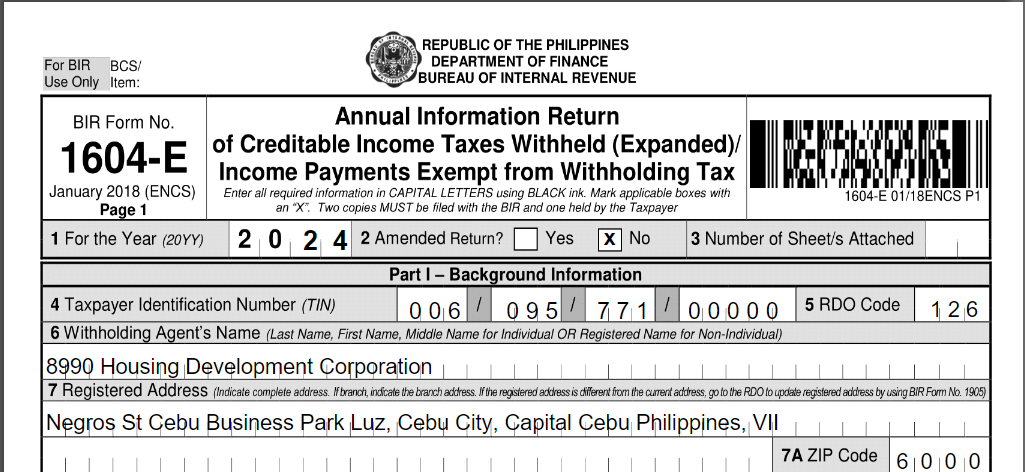

Form 1604-E is a tax form used in the Philippines for the annual filing of creditable withholding taxes on compensation. This form is utilized to report the total amount of taxes withheld by employers from the salaries and wages of their employees throughout the year. It ensures compliance with the Bureau of Internal Revenue (BIR) regulations, summarizing the annual withholding tax remittances. Employers submit this form to provide a comprehensive account of the taxes withheld, helping to ensure accurate reporting and remittance of employee income taxes.

To generate Form 1604 – E, here are the steps to follow:

Note: Deadline – March 1

Requirement – Annual Information Return of Creditable Income Taxes Withheld (Expanded)

Source: http://www.cleodu-cpas.com/index.php/bir-tax-deadlines

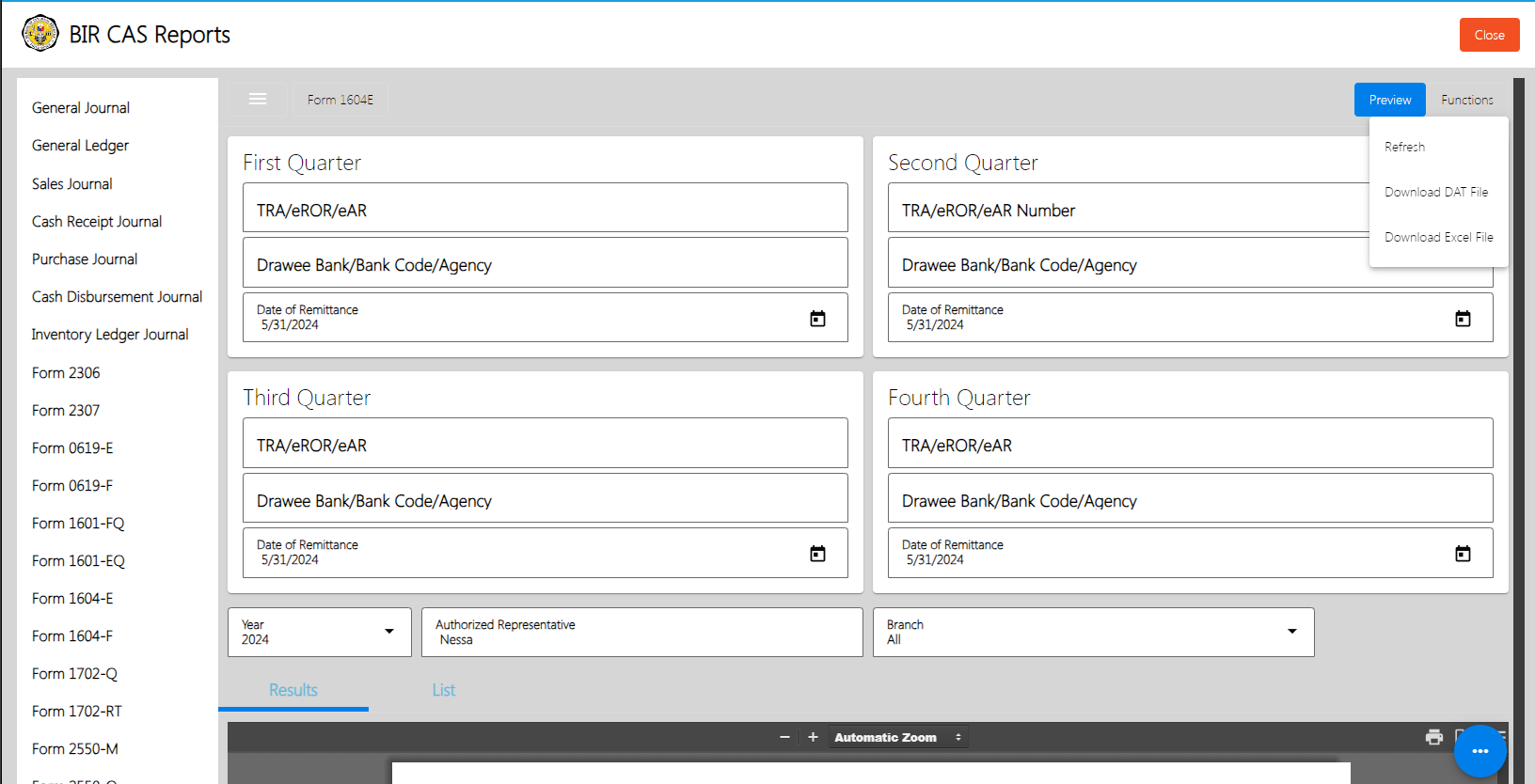

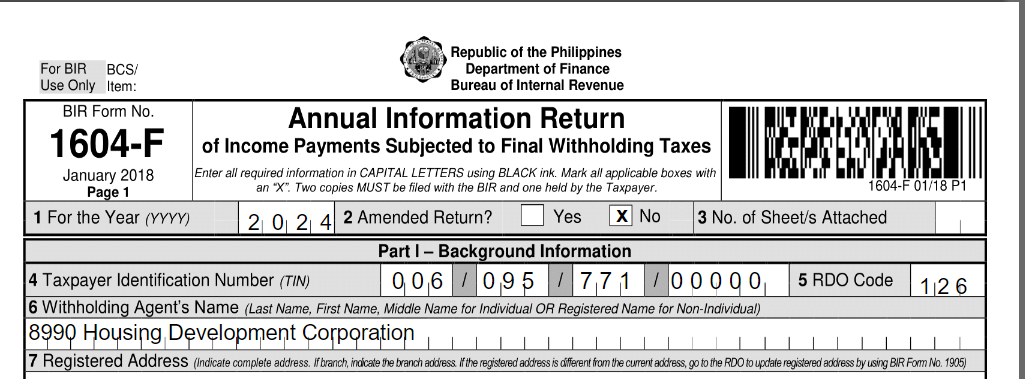

Form 1604-F is a tax form used in the Philippines for the annual filing of final withholding taxes. This form is used to report the total amount of taxes withheld on various income payments that are subject to final withholding tax, such as interest, dividends, and other specific types of income. It ensures compliance with the Bureau of Internal Revenue (BIR) regulations by summarizing the final withholding tax remittances for the year. By submitting this form, withholding agents provide a comprehensive account of the taxes withheld at source, ensuring accurate reporting and remittance of final income taxes.

To generate Form 1604 – F, here are the steps to follow:

Note: Deadline – On or before March 1 of the year following the calendar year

Requirement – Annual Information Return of Creditable Income TaxesWithheld (Expanded)/ Income Payments Exempt fromWithholding Tax

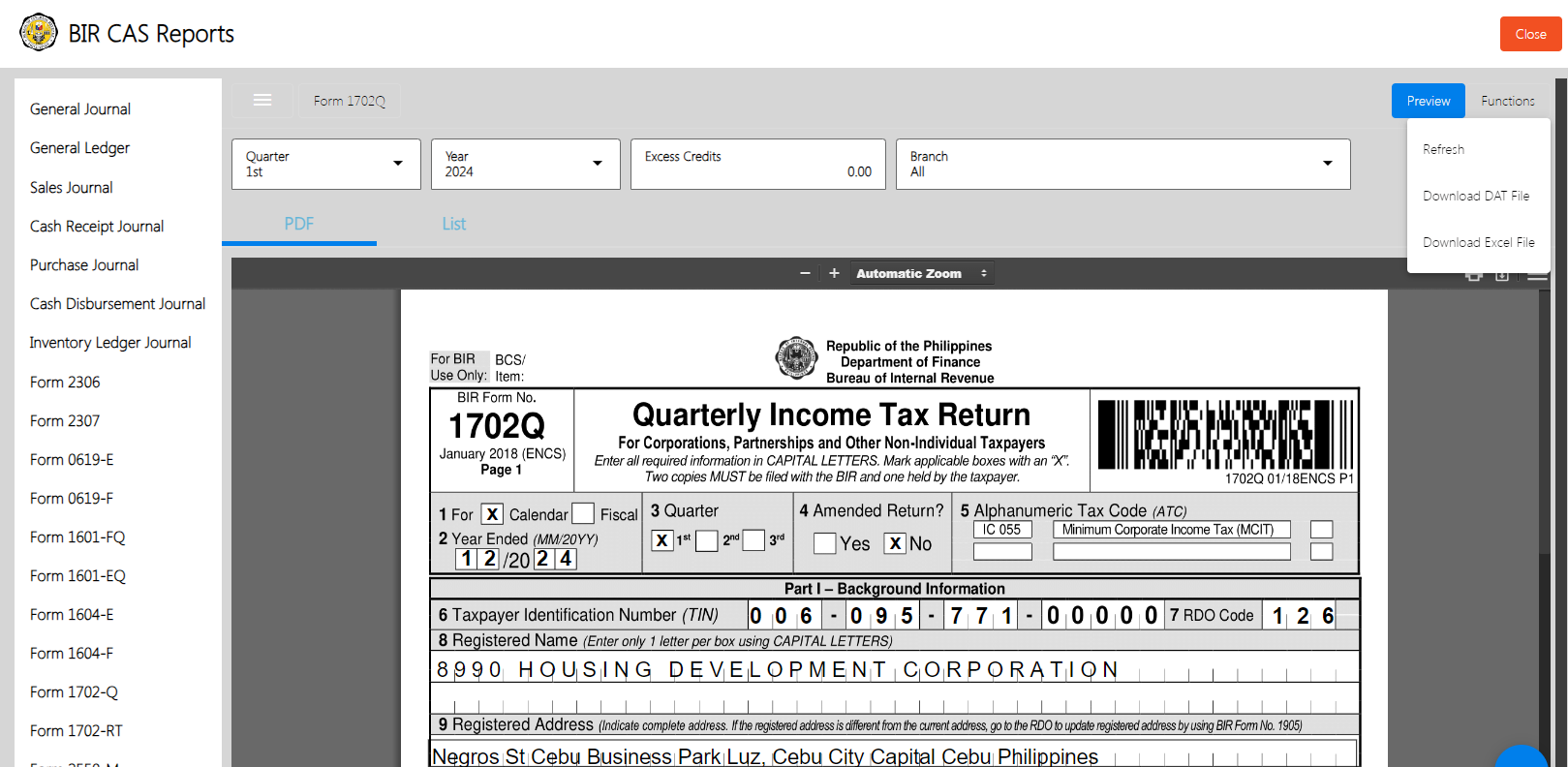

Form 1702-Q is a tax form used in the Philippines for the quarterly filing of income tax returns by corporations, partnerships, and other non-individual taxpayers. This form is designed to report the income earned and the corresponding taxes due for each quarter of the fiscal year. It ensures compliance with the Bureau of Internal Revenue (BIR) regulations, helping businesses to accurately document their quarterly income, allowable deductions, and tax liabilities. The form facilitates the timely payment of income taxes, thereby aiding in the proper monitoring and collection of corporate and partnership taxes by the BIR.

To generate Form 1702 – Q, here are the steps to follow:

Note: Deadline – Within sixty (60) days following the close of each of the first three (3) quarters of the taxable year whether calendar or fiscal year

Requirement – Quarterly Income Tax Return for Corporations,Partnerships and Other Non-Individual Taxpayers

Form 1702-RT is a tax form used in the Philippines for the annual filing of income tax returns by corporations, partnerships, and other non-individual taxpayers subject to the regular corporate income tax rate. This form is designed to report the annual income, allowable deductions, and the corresponding taxes due for the entire fiscal year. It ensures compliance with the Bureau of Internal Revenue (BIR) regulations by providing a detailed account of the taxpayer’s financial activities and tax obligations. By submitting Form 1702-RT, businesses help ensure accurate reporting and remittance of their annual income taxes, aiding in the proper monitoring and collection of taxes by the BIR.

To generate Form 1702 – RT, here are the steps to follow:

Note: Deadline – On or before the 15th day of the 4th month following close of the taxpayer’s taxable year

Requirement – Annual Income Tax Return for Corporation, Partnership And Other Non-Individual Taxpayer Subject Only toREGULAR Income Tax Rate

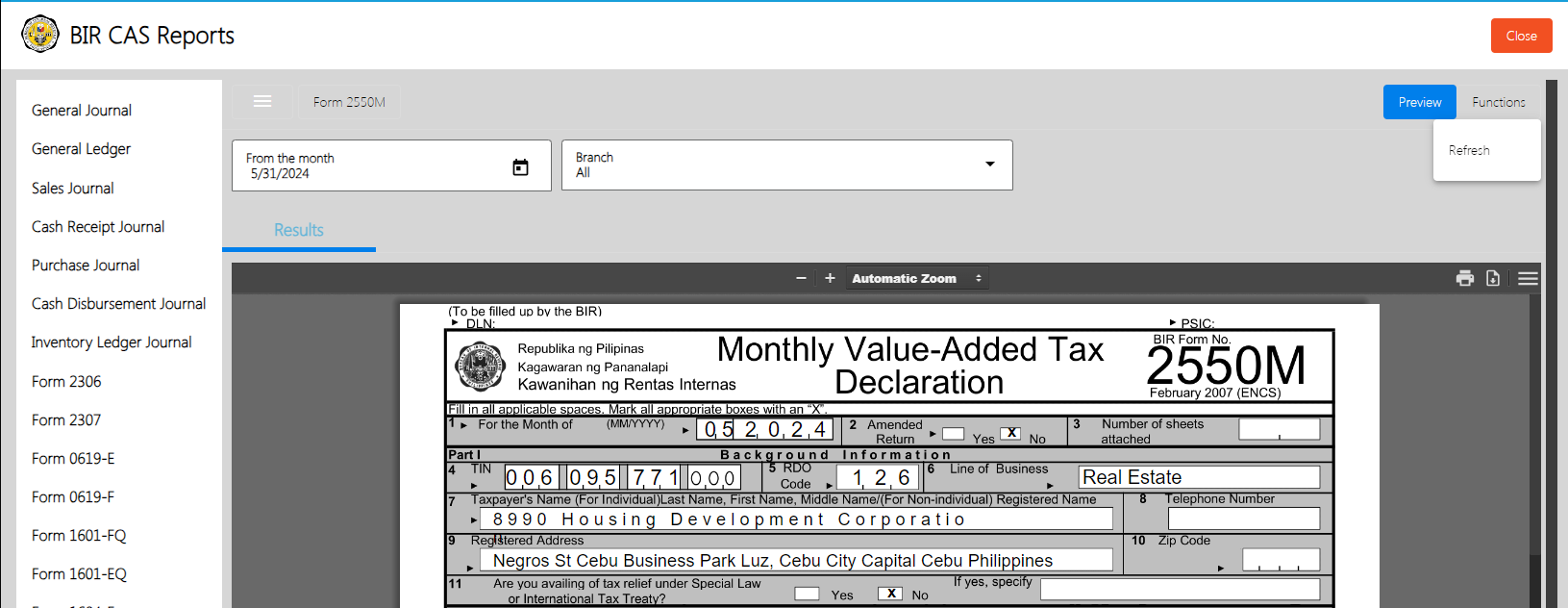

Form 2550-M is a tax form used in the Philippines for the monthly filing of value-added tax (VAT) returns. This form is designed to report the VAT payable for each month, including the details of sales, purchases, output VAT, and input VAT. It ensures compliance with the Bureau of Internal Revenue (BIR) regulations, helping businesses accurately document their monthly VAT transactions and obligations. By submitting Form 2550-M, taxpayers provide a comprehensive account of their VAT-related activities, facilitating the timely payment of VAT and aiding in the proper monitoring and collection of VAT by the BIR.

To generate Form 2550 – M, here are the steps to follow:

Note: Deadline – Not later than the 20th day following the close of the month

Requirement – Monthly Value-Added Tax Declaration

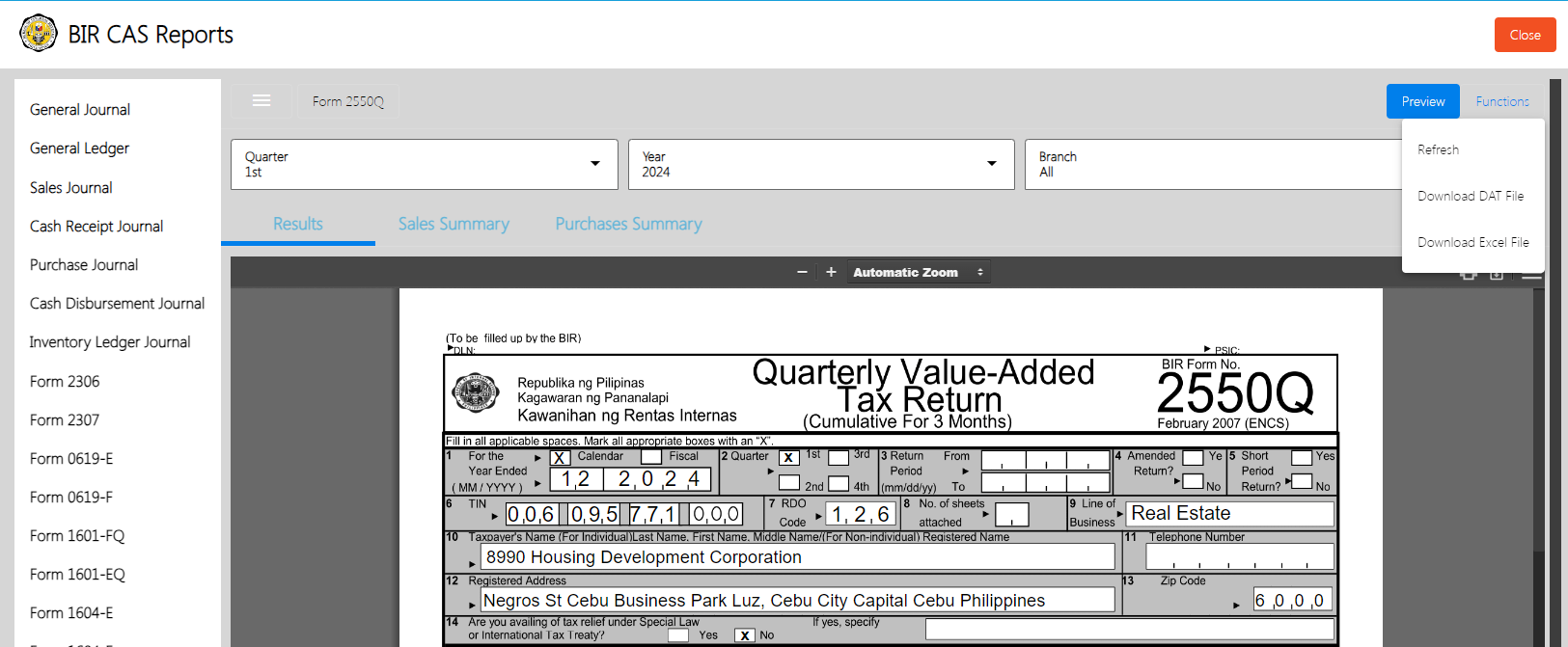

Form 2550-Q is a tax form used in the Philippines for the quarterly filing of value-added tax (VAT) returns. This form is designed to report the VAT payable for each quarter, including detailed information on sales, purchases, output VAT, and input VAT for the period. It ensures compliance with the Bureau of Internal Revenue (BIR) regulations by helping businesses accurately document their VAT transactions and obligations on a quarterly basis. By submitting Form 2550-Q, taxpayers provide a comprehensive account of their VAT-related activities, facilitating the accurate reporting and timely payment of VAT, and aiding the BIR in proper monitoring and collection of VAT.

To generate Form 2550 – M, here are the steps to follow:

Note: Deadline – Not later than the 25th day following the close of each taxable quarter

Requirement – Quarterly Value-Added Tax Return (Cumulative for 3 Months

Typically replies within a few hours

Log in to Messenger

Log in to Messenger